{kind=link}

TEVD helps retirees measure total retirement value by combining lifetime income, remaining assets, and long term security.

For decades, retirement planning has often been explained through a simple question: What return can my investments generate? While investment return is important, it does not fully answer the real question retirees care about most: How much economic value will my retirement strategy actually deliver over time?

That question becomes especially important for individuals approaching retirement with a 401(k), IRA, brokerage account, or other accumulated savings. A portfolio may look strong on paper, but if it does not create reliable income, preserve assets, reduce emotional stress, or support legacy goals, the traditional return number may not tell the full story.

This is why RESO Your Finances is introducing a new planning framework called Total Economic Value Delivered, or TEVD.

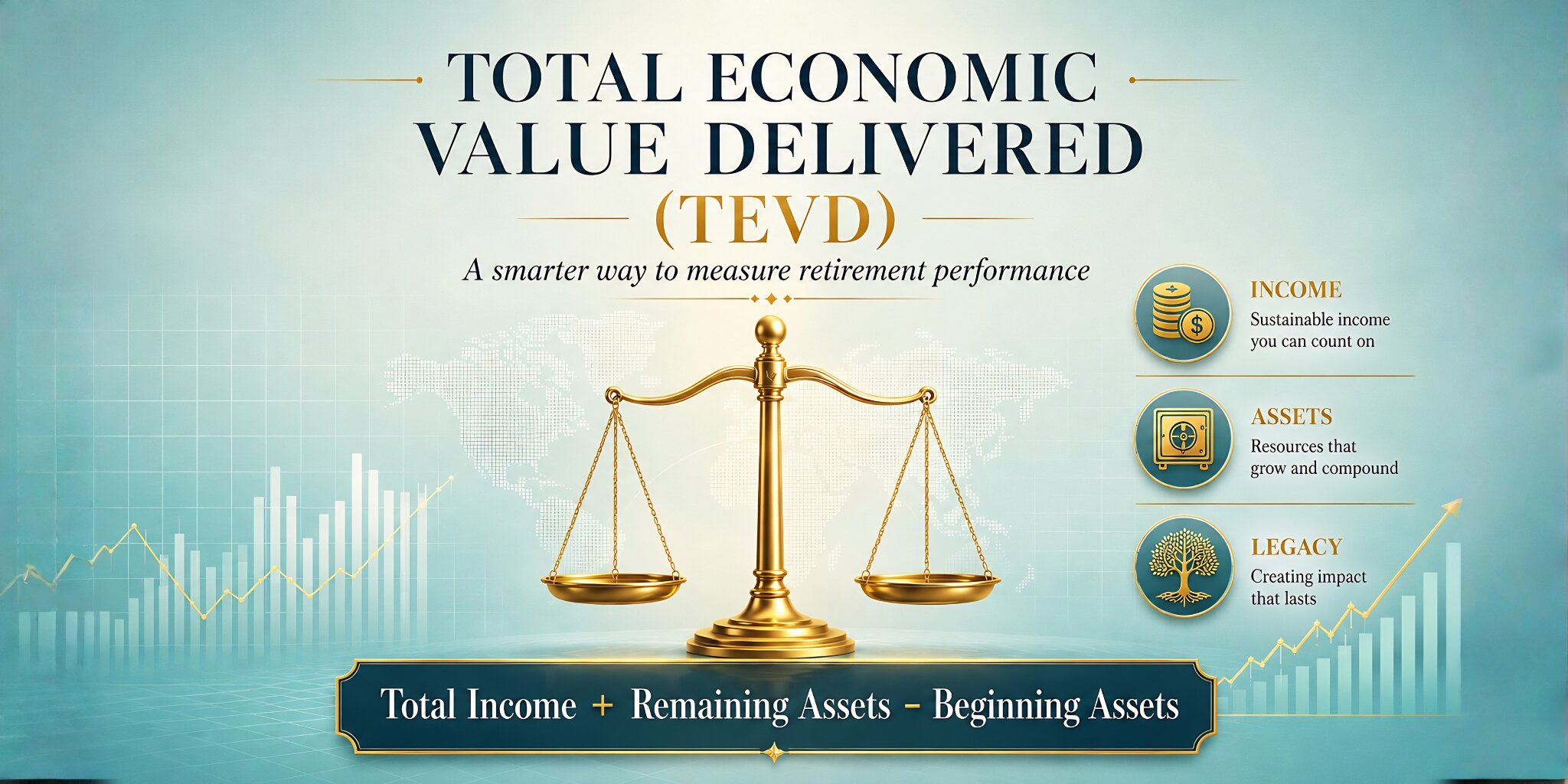

TEVD is designed to measure retirement performance in a more complete way by combining two critical elements: the income generated during retirement and the remaining assets available later in life. In simple terms, TEVD asks:

How much income did the strategy deliver, how much money remains, and how does that compare to the original starting capital?

The basic formula is:

TEVD = Total Retirement Income + Remaining Assets – Beginning Assets

This approach changes the conversation. Instead of only comparing investment returns, TEVD compares the total economic result delivered to the retiree and their family.

Why Traditional Retirement Metrics Are Incomplete

Most people understand investment performance as a percentage return. For example, if a portfolio earns 6% or 7%, that appears to be a good result. But retirement is different from accumulation.

During working years, the primary goal is often growth. During retirement, the goal becomes more complex. Retirees need income, stability, tax awareness, downside protection, inflation planning, and often some form of legacy preservation.

A traditional return figure does not show whether a strategy can provide dependable annual income. It does not show whether the retiree had to reduce spending during market downturns. It does not show whether assets were depleted too quickly. It also does not show whether there is money left at age 85, 90, or 95.

That is the gap TEVD is designed to address.

For example, two retirement strategies may begin with the same $500,000. One may generate higher income but leave little remaining value. Another may preserve more assets but provide income that is too low to support the retiree’s lifestyle. A third strategy may combine guaranteed income, market linked growth potential, and legacy preservation.

Without a broader measurement system, it is difficult to compare these outcomes fairly.

A Simple Example: The $500,000 Retirement Decision

Consider a 65 year old retiree with $500,000 in retirement savings.

A traditional withdrawal strategy based on the well known 4% rule might begin with approximately $20,000 per year in income. The advantage is flexibility and continued market participation. The challenge is that income depends on portfolio performance, sequence of return risk, future withdrawals, inflation, and how long the retiree lives.

Now compare that with a strategy designed to generate more structured retirement income. Depending on the product, age, payout structure, and market conditions, certain annuity based strategies may be designed to generate a higher annual income level than a traditional 4% withdrawal approach. Some strategies may also include features focused on lifetime income, asset retention, or death benefit protection.

TEVD does not simply ask, “Which strategy has the highest return?” It asks a more practical question:

By age 95, the key question becomes: how much total income was received, and how much value remains?

Assume a simplified illustration:

A retiree starts with $500,000 at age 65.

One traditional strategy generates $20,000 per year for 30 years, for total income of $600,000, and leaves $200,000 in remaining assets at age 95.

The TEVD would be:

$600,000 + $200,000 – $500,000 = $300,000

Now compare that with a higher income retirement strategy. Suppose it generates $34,000 per year for 30 years, for total income of $1,020,000, but because more income was distributed during retirement, it leaves only $100,000 in remaining value at age 95.

The TEVD would be:

$1,020,000 + $100,000 – $500,000 = $620,000

A third strategy may be designed to balance income and legacy. Suppose it generates $30,000 per year for 30 years, for total income of $900,000, and leaves $250,000 in remaining assets at age 95.

The TEVD would be:

$900,000 + $250,000 – $500,000 = $650,000

This simplified example shows why the framework matters. The highest income strategy is not automatically the best strategy. The most conservative strategy is not automatically the best strategy either.

TEVD helps compare the tradeoff between income received during retirement and assets remaining later in life. A strategy that produces the highest annual income may reduce future legacy value. A strategy that preserves more assets may provide too little income to maintain the retiree’s desired lifestyle.

The goal is not simply to maximize income or maximize remaining assets. The goal is to identify the strategy that delivers the strongest total economic value based on the retiree’s income needs, risk tolerance, longevity expectations, and legacy objectives.

That is the essence of TEVD.

Why TEVD Is Different

TEVD helps make retirement planning more visible, measurable, and client centered.

Many retirees do not think only in terms of investment return. They think in terms of lifestyle, security, family, and control. They want to know:

- Will I have enough income?

- Can I maintain my standard of living?

- What happens if I live longer than expected?

- Will my spouse be protected?

- Will there be something left for my children or beneficiaries?

- Am I taking too much market risk at the wrong time?

TEVD brings these questions into one measurable framework.

It is especially useful when comparing strategies that traditional performance reports may not evaluate properly. For example, a retirement strategy may include a combination of portfolio assets, guaranteed income products, indexed annuities, Roth conversion planning, life insurance with living benefits, or other financial tools. Each component may serve a different purpose.

One component may create income. Another may preserve capital. Another may help with taxes. Another may provide liquidity or legacy value. TEVD allows these components to be evaluated together rather than separately.

A Swiss Inspired View of Retirement

RESO Your Finances is built on a Swiss American planning philosophy. Switzerland’s retirement culture places strong emphasis on structured income, long term security, and disciplined capital planning. In the United States, many retirees are left to manage retirement risk on their own through 401(k)s and IRAs.

This creates a major challenge.

The American retirement system has shifted much of the responsibility from institutions to individuals. Many people now have retirement assets, but not necessarily a retirement income system. They may have accumulated savings, but they have not created their own personal pension structure.

TEVD supports this broader planning philosophy. It helps evaluate whether a retiree’s capital is simply invested, or whether it is organized to deliver income, protection, and long term value.

Why This Matters Now

The retirement landscape has changed. People are living longer. Traditional pensions are less common. Market volatility remains a concern. Inflation has reminded households that purchasing power can change quickly. Healthcare costs and long term care risks continue to affect retirement confidence.

In this environment, retirees need more than a portfolio statement. They need a clearer way to understand whether their financial strategy is truly delivering value.

TEVD can become a powerful tool for that conversation.

It does not replace professional financial planning. It does not eliminate risk. It does not guarantee that one strategy is always better than another. But it creates a more complete framework for comparing retirement outcomes.

For retirees and pre retirees, this can be a major step forward. It allows them to move beyond isolated numbers and evaluate what matters most: income received, assets preserved, and total value delivered over time.

The RESO Your Finances Difference

RESO Your Finances believes retirement planning should be measured by results that people can understand. A high performing strategy should not only look good in theory. It should support real life.

That means helping clients evaluate retirement income, asset preservation, tax efficiency, market exposure, family legacy, and long term confidence.

TEVD is part of that mission.

By introducing Total Economic Value Delivered, RESO Your Finances is helping retirees ask a better question:

Not simply, “What return did I earn?” but “What total economic value did my retirement strategy deliver?”

That distinction may become one of the most important differences in modern retirement planning.

RESO Your Finances offers a thoughtful approach to retirement planning that emphasizes income stability and long term adaptability. Connect with RESO Your Finances on LinkedIn, Facebook, YouTube, and Trustpilot.